Broad View on Swan Energy

A broad first look at a complex story where stock price momentum has faded and execution will now decide the future

In our ongoing search for companies that traded at exorbitant valuations last year but have since fallen sharply, Swan Energy emerged as an intriguing candidate. Initially, we were skeptical about allocating our research hours here due to persistent valuation discomfort, even after the recent stock price correction. However, we decided to dedicate a few hours to develop a broad understanding and see if the potential upside here justifies spending more time. This article outlines our preliminary thoughts and broad understanding; we welcome insights and corrections from our readers.

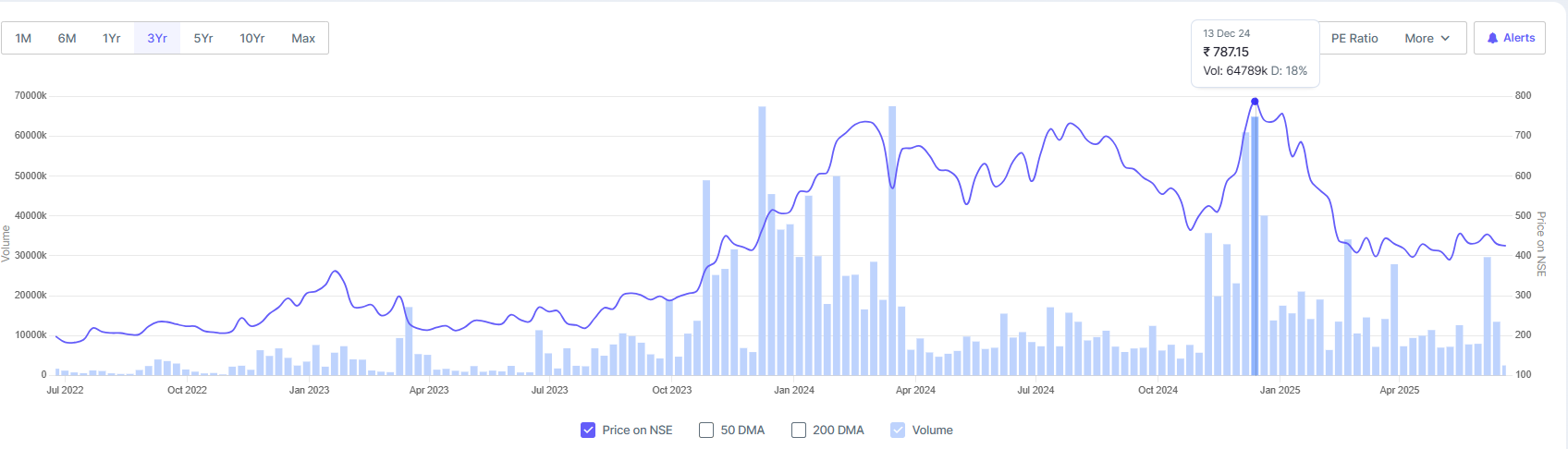

Swan Energy captured the market's imagination in CY23 and CY24, riding high on the optimism surrounding its strategic acquisition of Reliance Naval (now Swan Defence and Heavy Industires or SDHI).

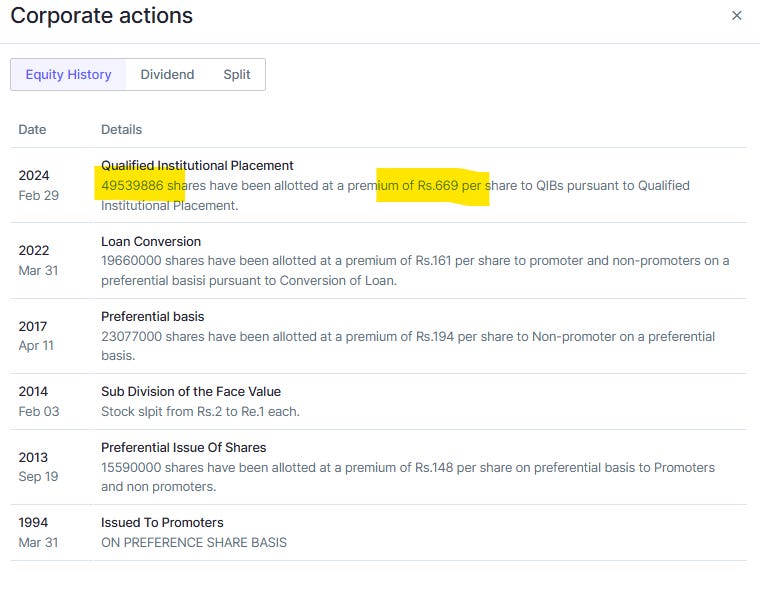

Backed by ambitious plans, the company successfully raised capital via a Qualified Institutional Placement (QIP) at valuations significantly higher than today’s market price. Many big and reputed institutional investors participated in this QIP.

Fast forward, the stock trades at nearly half of the QIP price, reflecting investor caution amid execution uncertainties. With this post, we try to understand the key moving parts of the business and what it means at the current market price.

Key Moving Parts

Swan Energy comprises three primary business verticals: LNG, Defence & Shipyard, and Veritas India (Petrochemical logistics). Ancillary operations like real estate and textiles exist but are minor contributors, lacking strategic significance in the broader corporate landscape.

LNG Business

Business Model: The LNG terminal business operates on a tolling model, where Swan earns revenues by charging customers a fixed fee per MMBTU of gas regasified. The business relies on long term "use-or-pay" contracts, offering stability but requiring timely completion and operational efficiency.

Initially, Swan's LNG terminal project at Jafrabad, Gujarat was planned around an innovative Floating Storage Regasification Unit (FSRU) model, boasting stable toll based revenues from long term "use-or-pay" contracts. However, repeated project delays triggered by unforeseen factors severely impacted timelines and economics. Ultimately, Swan was compelled to sell the FSRU to Turkey’s BOTAS in July 2024, realizing approximately USD 399 million, leading to a major reset in project economics.

As of now, only 39% of the onshore infrastructure is complete, leaving Swan dependent on fresh capital, strategic partnerships, and accelerated execution to meet its contractual obligations. This is where the March 2025 Heads of Agreement (HoA) with AG&P LNG (Singapore) becomes crucial.

Key points of the HoA include:

JV for LNG supply: A new sourcing company for LNG in India or elsewhere, with 51% stake held by Swan and 49% by AG&P.

Collaboration at terminal level: AG&P to support regasification and may take an equity stake in Swan’s LNG terminal (SLPL).

JV for vessel operations: To jointly procure and operate FSRU and FSU assets, where AG&P will hold 51% stake and Swan 49%.

While these agreements are subject to due diligence, they suggest clear strategic alignment and intent to revive the stalled terminal. If Swan completes Phase I (5 MMTPA) with AG&P’s support, annual revenues could range from INR 800–1,000 crore, with EBITDA margins of 60–70%. However the attributable profit to Swan Energy will lower considering AG&P share in the business and potential dilution (if any).

Swan Defence and Heavy Industires Ltd: Shipyard and Defence Business

Business Model: Swan's Defence and Shipyard segment revolves around the construction, maintenance, and refurbishment of naval and commercial vessels. The model depends heavily on securing long term defence contracts and commercial shipbuilding orders, both involving extended gestation periods and lumpy cash flows.

Acquired through NCLT proceedings, the Pipavav shipyard (formerly Reliance Naval) positions Swan as a significant player in India's defence and commercial shipbuilding landscape. With a 740 meter dry dock, the largest in India, Swan could theoretically build or maintain large vessels, positioning it ahead of established players such as Cochin Shipyard, Garden Reach, and Mazagon Dock in sheer capacity terms.

However, size alone doesn’t guarantee utilization. Shipbuilding, particularly defence related, involves extensive lead times, rigorous bidding, and inherently cyclical orders. While promoters are considered to have favorable ties with the current political regime, it is widely expected by the street that the company will be able to procure good amount of orders from various defence departments.

Given peer valuations such as Cochin Shipyard (market cap ~ INR 57,000 crore), GRSE (~ INR 36,000 crore), and Mazagon Dock (~ INR 1,33,000 crore), the upside for SDHI can be substantial. This entity was recently listed and is currently in the price discovery phase. If the company manages to refurbish the shipyard on time, secure a meaningful pipeline of defence and commercial shipbuilding orders, and build a solid execution track record, SDHI could evolve into a significant value driver and potentially a major wealth creation engine for Swan Energy. That said, these outcomes remain execution dependent and will take time to materialise.

Veritas India (Petrochemical Logistics Business)

Business Model: Veritas operates a petrochemical logistics terminal business in UAE's Hamriyah Free Zone, earning revenue through storage, blending, distillation/fractionation, and value added services. The model thrives on infrastructure led, recurring logistics and service fees.

Operating through Verasco FZE in UAE’s Hamriyah Free Zone, Veritas India uniquely blends petrochemical logistics, distillation/fractionation, storage, blending, and drumming—positioning it distinctively within the Middle Eastern terminal landscape. With 170,000 CBM storage, it generates stable, logistics led revenue streams primarily from traders and refiners.

Despite its differentiated offerings (notably the only regional facility offering fractionation), Veritas’ growth visibility remains moderate. The success heavily depends on sustained demand from petrochemical traders and clients requiring customised blending services. Nonetheless, this business remains profitable and provides steady operational cash flows. There is not much information available on the future growth opportunities.

Ancillary Businesses: Not Material

Swan's additional ventures into real estate and textiles, once meaningful, are now strategically peripheral, with minimal impact on overall valuations or corporate strategy. Investors should regard these businesses as legacy segments rather than value drivers.

Conclusion: Execution is Everything

Swan Energy’s narrative remains enticing: ambitious plans, substantial assets, strategic acquisitions, and promoters with seemingly robust connections to be able to secure good orders. However, for past QIP investors, the story has thus far been disappointing due to project delays, compromised LNG economics from the forced FSRU sale, and prolonged uncertainty in realizing strategic ambitions.

In a blue sky scenario where Swan executes its key projects timely and scales effectively, revenue and profitability can grow multifold from the present levels, creating substantial wealth for shareholders. However, it is a high risk, execution intensive journey ahead. Swan has ample cash reserves and influential promoters, but the risk profile remains elevated for a super reward.

For us, it is not suitable at this stage since we are on the lookout for asymmetric setups where the reward is high and the risk of losing capital is low. That said, we remain open to changing our views with more information and consistent execution progress from the company.

Important Note and Disclaimer: Please note that this note is shared only for the education purpose and in no way, it constitutes any buying or selling recommendation. We do not hold Swan Energy and Swan Defence in our portfolio.

If you are interested in accessing our research and joining a network of well informed investors, please contact us at Gaurav.a@nineonecapital.in