Creative Graphics: A Case Study in Investing Through Market Discomfort

How cash flows, execution, and valuation converge in a small-cap transition story

Let’s be honest, buying small caps right now feels terrible. The screens are red, liquidity is drying up, and everyone is running for the exits. But that’s exactly when you find the mispriced bets.

Over long periods of investing, we have found that the best opportunities rarely appear when markets are comfortable. They tend to emerge when visibility is low, sentiment is weak, and short-term uncertainty dominates decision making.

Against this backdrop, we are sharing one investment idea where we have spent considerable time on research and analysis. Our intention is to present our thinking transparently and allow readers to benefit from the work we have done. As always, this note is shared strictly for educational purposes and should not be construed as an investment recommendation.

We’ve been tracking Creative Graphics Solutions for a while, and the current bad market for microcaps is offering this business at a great valuation. Markets are treating it like just another beaten-down microcap. They’re missing the actual story.

What makes this opportunity particularly interesting is that it sits at the intersection of two factors that markets often misprice during corrections.

The Mental Model and Introduction to the Company

We find that using simple mental models helps in making sense of complex businesses, especially during phases when markets are volatile and narratives are noisy. In the case of the company discussed in this note, the mental model is straightforward and intuitive. At the core is a stable operating business that generates steady cash flows. Alongside this sits a higher growth opportunity that can be scaled using internal resources, without stretching the balance sheet or relying excessively on external capital.

This framework allows us to assess the business in a structured manner: first by understanding the strength and durability of the core operations, and then by evaluating how incremental capital is being deployed to create future growth.

The company we are talking about is Creative Graphics Solutions India Ltd.

The company fits this model well. It operates a mature, cash generative flexography business that provides stability and financial support, while simultaneously building a pharmaceutical packaging platform that has the potential to scale meaningfully over time.

The interaction between these two segments, one providing cash flow and the other absorbing it for growth, is central to our investment thesis. In the sections that follow, we first discuss the cash generating core business, and then outline how the growth engine is being built on top of it.

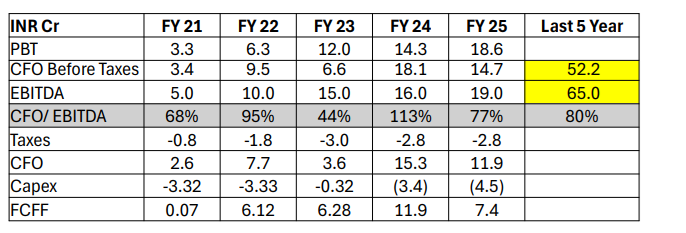

The Cash Engine: Flexography Business

The flexography business forms the foundation of the company’s financial stability. It operates in a critical but largely invisible part of the packaging value chain, supplying flexographic printing plates used by packaging converters serving FMCG and pharmaceutical clients. While end consumers rarely see this layer, it plays a decisive role in print quality, efficiency, and wastage control.

What makes this business structurally attractive is its predictability. Customer relationships tend to be long-term, switching costs are meaningful, and order flows are repeat in nature. Once a printer is qualified and integrated into a client’s workflow, replacement is neither easy nor economical.

Over the past few years, the business has consistently demonstrated strong conversion of operating profits into cash flows. This is driven by a combination of steady demand, limited maintenance capex requirements, and disciplined working capital management. As a result, the business is able to generate meaningful free cash flows even in moderate growth scenarios.

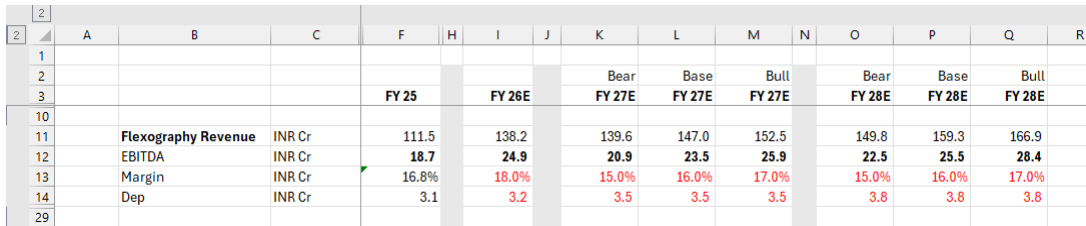

From a forward looking perspective, we have laid out revenue and margin assumptions across base, bull, and bear cases over the next two years. Even under conservative assumptions, the business is expected to grow at a steady pace, with margins remaining resilient. In the base case, flexography revenues grow in line with industry demand, while margins remain stable. In the bull case, operating leverage and better utilization drive incremental margin expansion.

What is particularly noteworthy is that, on a post-tax basis, the flexography segment is expected to generate approximately ~₹12-13 crore of free cash flow annually without requiring any major incremental capital investment. This provides a strong internal funding source for the company’s growth initiatives.

There is also a structural growth tailwind at play. The business has begun expanding internationally, with the first overseas line commissioned in Oman. The operating model here is efficient whcih is to design and pre-press work continues to be done in India, while manufacturing is closer to the end customer, allowing for both cost efficiency and faster turnaround times.

Additionally, regulatory shifts such as the implementation of Extended Producer Responsibility (EPR) norms are structurally favorable for flexography. Flexo printing is better suited for recyclable and thinner substrates, particularly compared to traditional printing methods that require thicker films. As packaging moves toward sustainability-led designs, this creates a natural demand tailwind for flexography-based solutions.

Importantly, even under optimistic assumptions, we have remained conservative in factoring growth from this segment. The flexography business is not being valued as a high-growth engine, but rather as a stable cash generator with embedded optionality, a characteristic that adds resilience to the overall investment thesis.

The Growth Engine: Pharmaceutical Packaging

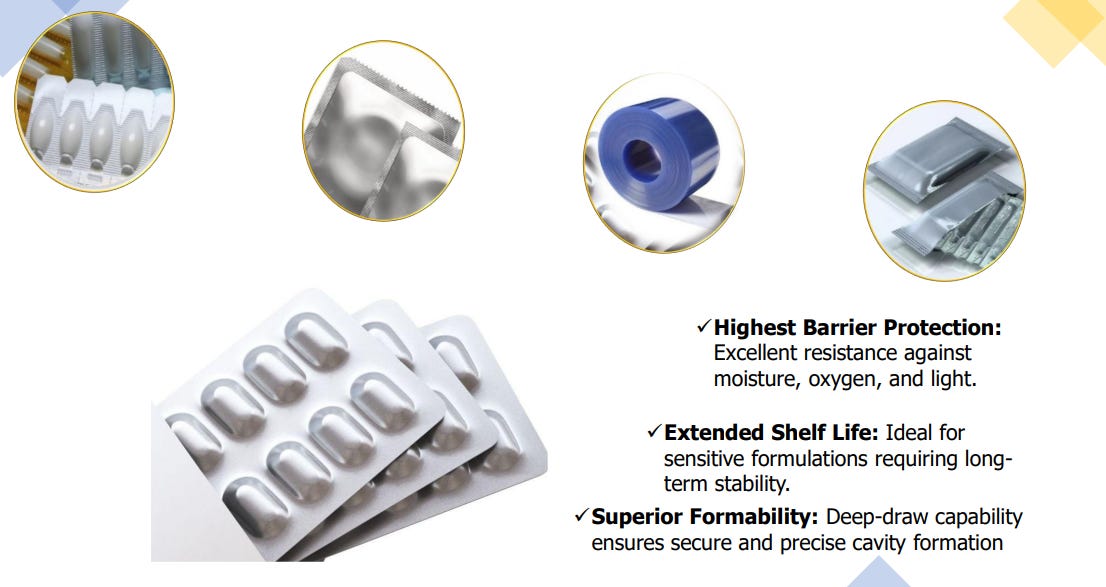

The second leg of the company’s growth strategy lies in pharmaceutical packaging, specifically in high barrier formats such as Alu-Alu and PVDC-coated films. This is a structurally attractive segment, but one that is difficult to enter and even harder to scale without deep process discipline.

The Indian Alu-Alu market itself is sizeable, estimated at over 60,000 tonnes annually and growing at a low to mid teens rate. Historically, it has been dominated by a handful of established players with long-standing customer relationships and high technical entry barriers. Product quality, process consistency, and regulatory compliance matter far more than pricing alone, which has kept the market relatively consolidated despite its attractive economics.

What makes this segment particularly challenging is the nature of customer validation. In pharmaceutical packaging, failures are not immediately visible. Issues such as pinholes, sealing defects, or moisture ingress often show up months later during stability testing. As a result, customers take 12 to18 months to qualify a new supplier, and once approved, are extremely reluctant to switch. This creates high entry barriers but also strong long-term stickiness for vendors who manage to cross the qualification phase.

Wahren’s progress needs to be viewed in this context.

Despite being a relatively new entrant, the company has been able to enter accounts that were earlier serviced by entrenched suppliers. The company has already onboarded several established pharmaceutical clients and is in the process of getting approvals from larger players, which could materially expand its addressable opportunity over the next few years.

An important nuance here is the structure of the market. Branded pharma companies are highly quality conscious and tend to be sticky once satisfied, while CDMO and contract manufacturers are more price sensitive but allow faster volume ramp up. Wahren has approached the market pragmatically, building volumes first and gradually moving up the value chain as product performance stabilises.

The early results of this approach are visible. Within a relatively short period, the company has been able to scale market share to mid-single digits while maintaining reasonable profitability. A key extension of this strategy is the entry into PVDC-coated films. PVDC plays a complementary role to Alu-Alu, offering high moisture and oxygen protection while allowing visual inspection of the tablet. Demand for PVDC has been rising due to tighter export regulations, longer shelf-life requirements, and increasing preference for sustainable packaging formats.

The strategic importance of PVDC lies in two areas. First, it allows the company to offer a wider product basket to the same pharmaceutical clients, improving wallet share and customer stickiness. Second, it significantly expands the addressable market without materially increasing customer acquisition costs.

The company’s entry into PVDC has also been capital efficient. Through an NCLT acquisition, it secured a high-quality German coating line at a fraction of replacement cost. This provides a meaningful cost advantage versus new entrants and enables competitive pricing without sacrificing margins. At peak utilisation, this line alone has the potential to generate meaningful revenue with healthy EBITDA margins.

Taken together, the pharma packaging business represents a classic case of difficult execution but high long-term reward. The market is unforgiving to new entrants, but once scale and quality are established, it offers durable growth, pricing power, and strong customer stickiness.

At this stage, Wahren appears to be past the most difficult phase of entry and validation. The next phase is one of scaling volumes, deepening customer relationships, and improving operating leverage. All of these factors can materially change the earnings profile of the business over the next few years as reflected below:

Capital Requirement and No Equity Raising Requirement

One of the key aspects we focus on while evaluating micro and small-cap companies is how growth is funded. This becomes especially important in this segment because many businesses remain dependent on external capital to scale. When markets are supportive, this dependency often goes unnoticed. During corrections, however, it becomes a major constraint and one of the primary reasons microcaps tend to underperform. In the current environment, this distinction matters even more.

The pharmaceutical packaging business here is working-capital intensive by nature, given the need to hold inventory and service large, regulated customers with longer credit cycles. As the business scales, funding requirements inevitably increase. What we have evaluated closely is whether this growth can be supported in a disciplined manner, without creating balance sheet stress or excessive reliance on equity dilution.

Based on our analysis, the company’s growth plan is largely funded through internal accruals, with only a limited requirement for external funding. A significant portion of the capital needed to support expansion is expected to come from cash generated by the core business, while the balance is planned to be met through measured debt rather than equity issuance.

We have laid out the detailed funding math, assumptions, and sensitivities in the report that we have prepared for our clients. The key takeaway, however, is that the company does not appear structurally dependent on favourable market conditions to execute its growth plans. As scale improves, working capital efficiency is also expected to improve, further easing funding pressure over time.

This aspect is particularly important in the current market environment. Businesses that can fund growth internally tend to navigate downcycles far better than those reliant on capital markets. In our view, this capital discipline meaningfully reduces downside risk while allowing the company to continue compounding through the cycle.

Valuation and Forward Scenarios

We believe no investment discussion is complete without a clear view on valuation. While business quality and execution are critical, the price paid ultimately determines long-term outcomes.

From a valuation perspective, we prefer to assess this business through a medium-term lens rather than anchoring to near-term volatility. The company is currently in a transition phase, where reported numbers do not yet fully reflect the operating leverage that is likely to emerge as capacity utilization improves and the business mix continues to evolve.

In the detailed valuation framework presented in our report, we have laid out both bull and bear case scenarios to account for execution variability and near-term uncertainty. These scenarios incorporate different assumptions around utilization levels, margin progression, and growth trajectories, allowing us to evaluate outcomes across a wide range of possibilities rather than relying on a single-point estimate.

Based on these scenarios, the stock currently trades in the range of approximately 10x to 6x FY27 earnings, depending on the operating assumptions applied. As our readers are aware, we generally prefer investing in businesses that are available at reasonable valuations on current earnings, with upside driven by execution rather than multiple expansion. At present, Creative Graphics trades at approximately 15x trailing earnings, which, in our view, provides a reasonable margin of safety given the business profile and growth visibility.

This valuation does not, in our assessment, fully reflect the structural improvement in business quality or the earnings potential as the pharmaceutical packaging segment scales over the next few years.

Key Risks

As with any investment, risks remain and must be acknowledged clearly.

1. Raw Material Lag Effect: The primary risk to near-term profitability isn’t the inability to pass on costs, but the timing of it. While the company has a pass-through mechanism for Aluminum, it does not happen instantaneously. In a scenario of continuous or sharp price hikes, the company is forced to service existing order books at higher procurement costs before new pricing takes effect.

2. Working Capital Intensity: The aggressive shift from smaller players to Tier-1 pharmaceutical clients (e.g., Torrent, Aurobindo) validates the product quality but structurally alters the cash cycle. These large incumbents demand standard 90-day credit terms, significantly stretching the receivables cycle compared to the cash-rich Flexo business.

3. Execution Risk: If the ramp-up to the targeted 70-80% utilization takes longer than the projected 12-18 months due to stickier customer qualification cycles, the anticipated expansion in blended margins will be delayed, leaving the company dependent on the lower-margin core for longer than expected

4. Forex & Import Sensitivity: A significant portion of raw materials and capital machinery is imported, meaning a strengthening USD directly impacts procurement costs. While the company targets 20% export revenue by FY27 to create a natural hedge, current export volumes may not yet fully offset this import risk.

Closing Thoughts

We are sharing this analysis at a time when market sentiment remains cautious and visibility is limited. That is intentional.

In our experience, long-term outcomes are shaped not by timing the market, but by identifying businesses with sound economics, disciplined management, and the ability to compound through cycles.

A detailed investment note, including our factory visit observations and financial analysis, is available on our web portal for our clients. This note is intended to provide transparency into our thinking process and how we evaluate opportunities during the current challenging phases of the market cycle.

The approach outlined in this note reflects how we think about investing across market cycles, with an emphasis on discipline, business fundamentals, and long-term risk–reward rather than short-term market movements. For readers who would like to better understand our research process, how we evaluate businesses during volatile phases, or how our advisory approach is structured around capital preservation and long-term compounding, you may write to us at gaurav.a@nineonecapital.in or fill in the form here (link).

Important Note and Disclaimer: This article is not a buy/sell recommendation. This note is shared only for the education purpose and in no way, it constitutes any buying or selling recommendation.

Incredible gist just listening to your FirsT podcast with Shashank and really I feel you’re nailing it and crystal clear in your thoughts and words of speech more than that this Substack article you penned your analysis and assessed is in turn proves your versatility and know-how of the business right from its RootZ.

Great growing n share your wisdom - GaurAv AgArWal.

Very well written... Thanks for helping the investing community

Kindly, also consider to touch upon competition