E2E Networks Vs Sanghvi Movers: Insights

When assets age fast and ROEs stay low, even growth stories face gravity

On the surface, comparing a traditional crane renting business with a modern GPU renting operation might seem like comparing apples and oranges. Yet, beneath the surface, the core economic principles are remarkably similar: invest heavily in expensive assets, rent them out over their useful life, and then discard or sell off the assets once they've served their purpose.

Similar Foundations, Different Timelines

Both businesses rely on asset utilization. An expensive asset, whether a massive crane or a cutting edge GPU, must recover its initial investment and generate returns during its operational lifetime. This core metric determines the Internal Rate of Return (IRR), a critical measure for evaluating the investment’s profitability.

However, there's one stark difference: lifespan. For cranes used by Sanghvi Movers, the useful life spans an extensive 35 to 40 years. Conversely, GPUs, such as those utilized by E2E Networks, face rapid technological obsolescence and typically have a useful life of just 3 to 4 years. This shortened lifespan places heightened importance on swiftly recovering investment and ensuring favorable market conditions remain steady.

Compare that with Sanghvi, with a long asset life, recovery is stretched over decades which provides more buffer for cycles, economic shifts, or even pricing corrections.

The GPU Challenge: Shorter Life, Higher Sensitivity

GPUs become obsolete quickly due to continuous technological advancements, improved power efficiency, and shifting workload demands. E2E Networks currently operates around 3700 Cloud GPUs, comprising models like H100, H200, A100, among others, emphasizing their strong market position in AI focused infrastructure.

Considering this rapid pace of obsolescence, we conducted a pretax IRR analysis under various scenarios, taking historical asset turnover rates and EBITDA margins as inputs with life of GPUs ranging from 3 to 4 years:

These scenarios illustrate significant sensitivity to the asset’s lifespan, even with constant asset turnover and EBITDA margins. Although management has extended depreciation policies from 3 to 6 years, realistically, GPUs are most effective and economically viable within 3 to 4 years, if not shorter due to accelerating technological advancements.

Stability vs Volatility: Crane Business for Comparison

In contrast, Sanghvi Movers’ crane rental business presents a different dynamic. With assets lasting around 35 years and assuming a net payback of approximately 7.5% per year, the pretax IRR is typically around 13 to14%.

It is important to note that we are not suggesting investing in Sanghvi Movers specifically; rather, the company serves as an example to illustrate how longer lived assets affect business model dynamics and IRR outcomes.

Valuation Perspective on E2E Networks

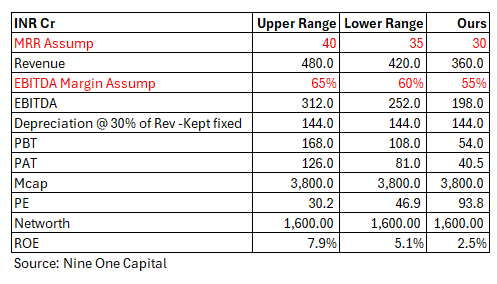

As of today, E2E Networks trades at a market capitalization of approximately INR 3800 crores, with around INR 1400 crores of cash. The management has aggressively guided an increase in monthly recurring revenue (MRR) from INR 10 crores per month to INR 35 to 40 crores. Even at the upper end of this optimistic guidance, E2E appears to be trading at approximately 30x earnings, yielding a modest ROE of around just 8%.

Even under these bullish assumptions, the return metrics appear underwhelming, suggesting an investment at current valuations primarily relies on the greater fool theory, where future returns depend heavily on another investor paying a higher price. This quote from our repository makes a perfect sense here: "Valuations are like teenage emotions: intense, short lived, and almost never rational."

Risk Reward Balance

At our core, we aim to earn solid returns under base case scenarios without risking capital in bear case outcomes. As Howard Marks says, "the most important thing is not making the most money when things go right but losing the least when they go wrong." When we look at asset heavy, short lifespan businesses like GPU rentals, the range of outcomes widens considerably.

With respect to E2E, even in the bull case seems to a sub-par investment while carrying a high risk if market conditions shift unfavorably (bear case).

If you found this analysis useful, do help us spread the word. Share it with friends, investors, or fellow thinkers who appreciate deep, independent research.

If you are interested in accessing our research and joining a network of well-informed investors, please contact us at Gaurav.a@nineonecapital.in