Good Results. Falling Stocks.

Markets eventually recognise operating performance. The challenge is surviving the waiting period.

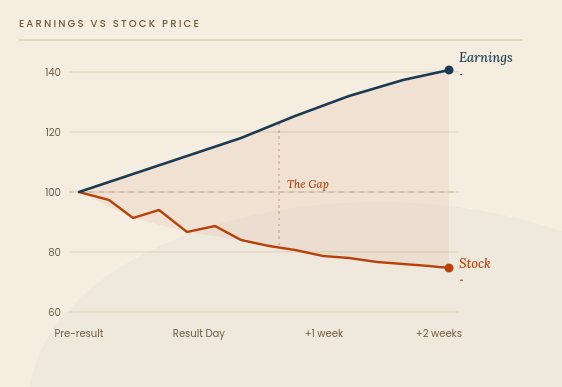

So far in Q4 FY26, four companies from our recommendation list have reported results. All four have delivered stellar numbers: strong revenue growth, healthy margins, clean cash flow conversion, and confident forward guidance. By every measure that matters to a business owner, these companies did exactly what we expected them to do. Now the valuations also on the trailing 12M basis are attractive with PE at around 10-12 for non BFSI and financial companies below 1x book value. However, the stock prices of these have not responded as shown below:

As shown, there is a substantial gap between the business performance and stock price performance. This is the gap we want to talk about today:

What the market is buying right now

Capital in the Indian market today is flowing into a narrow set of themes. Semiconductors, Data Centers, Defence, AI value chain, Nuclear, Capex-linked engineering names that fit the precision manufacturing narrative. Anything with a press release mentioning data centres or strategic capability has had a re-rating before the earnings have caught up.

We are not against any of these themes. Several of them have genuine tailwinds and real order books. The point is when a single basket of narratives consumes most of the marginal flow in the market, everything outside that basket gets sold or, more commonly, simply ignored. Volumes thin out, follow up buying doesn’t happen and good results are sold into by investors. Promoters wonder why a 25% earnings print earns a 5-10% fall on result day.

Why we are not surprised

Our framework is built around four buckets: high growth at a reasonable price, structurally strong businesses going through temporary headwinds, cyclicals near the bottom of their cycle at dirt cheap valuations, and deep value. Three of those four buckets are explicitly designed to find businesses that the market is not currently interested in.

So when we see operating performance improve and stock prices go the other way, our first instinct is not panic. It is to recheck our thesis, and ask ourselves: Are the numbers real? Is cash flow tracking the P&L? Has the competitive position changed? Is management still executing on what they guided?

In all four cases this quarter, the answer is yes.

The trap most investors fall into right here

This is precisely the point in the cycle when most investors abandon their strategy. The pain of holding underperformers while a different set of stocks runs vertical becomes psychologically intolerable. They sell what is working operationally but not on the screen, and rotate into whatever theme has already moved or going up. They convince themselves it is a fresh start, a smarter allocation, a recognition of changed market structure.

It is almost always the capitulation phase.

The investors switching strategy at this stage are not early. They are the last buyers of a theme that has already discounted years of future earnings, and the first sellers of businesses that are about to get their re-rating. This pattern repeats with painful regularity in Indian small caps. The names being sold today to buy today’s hot trade tend to be the names that lead the next leg up, while the trade being chased tends to peak within a few weeks/ months of the rotation.

We have written before about how sentiment and liquidity, more than fundamentals, drive valuations in the micro and small cap segment over short and medium horizons (link here). We are living that piece in real time right now. The businesses we own are compounding earnings. The market is choosing not to pay for that compounding yet because flows are elsewhere.

The honest difficulty is this: sentiment shifts are only visible in the rearview mirror. We get to know the change after a lag, sometimes several weeks, sometimes a couple of quarters. That is why we cannot promise to jump out at the top and jump back in at the bottom. Nobody in this segment can, despite what they claim on Twitter. What we can do is own the right businesses at the right prices, track them closely, and stay put until the cycle does its work.

“The big money is not in the buying and the selling, but in the waiting.” - Charlie Munger

We keep this in mind because the temptation to act, to do something, to feel busy, is strongest exactly when doing nothing is the correct decision. Strategies do not fail because they were wrong. They fail because the people running them abandoned them at the point of maximum discomfort, which is usually the point of maximum opportunity. Sticking to a time-tested process is not a personality trait. It is the entire edge. Once we start drifting with sentiment, we become indistinguishable from the crowd we are trying to outperform, and we lose the only thing that has worked for us across cycles.

Business Vs Stock Price

There is a distinction that often gets blurred in periods like this. A business compounds when revenue, earnings, free cash flow, return on capital, and reinvestment opportunity all move in the right direction over multiple years. A stock price compounds when the market chooses to recognise that business compounding through a higher multiple. The two are correlated over the long run. They are not correlated quarter to quarter, and often not even year to year.

We have seen this pattern many times in Indian small caps. Between 2011 and 2013, a long list of high quality businesses kept growing earnings while their stock prices did nothing. By 2014 to 2017, those same names had compounded multiple times over. The earnings were always there. The price simply caught up later, all at once. The same pattern played out after the small cap winter of 2018, and again selectively in 2022 and early 2023. The lesson from every one of these episodes is the same. Earnings compounding leads. Price compounding follows. Sometimes the lag is six months. Sometimes it is two years. It is never permanent. A company with growing earnings and clean cash flow eventually gets its price discovered. The market is slow, not blind.

What we are doing

We are continuing to hold. In some cases, we are adding. We are not adding because we are stubborn. We are adding because the spread between operating reality and market price is wider today than it was at the time of our original recommendation.

The companies in question are doing the work and the work is visible in the quarterly results. The unglamorous operational milestones that eventually convert into a re-rating are happening at the time of writing this note.

Our job in this part of the cycle is not to outsmart the market on what it wants to own next month. Our job is to make sure the businesses we own are still the businesses we wanted to buy and the underlying thesis is intact. If it is there, we are okay to hold.

Selling a business that is operationally on track because the screen is red is not risk management. It is locking in a permanent loss to escape a temporary discomfort.

Closing thought

The four companies referenced in this post will, in our view, look very different on a price chart twelve to twenty four months from now. We are not making a call on when the market will pay attention. We are making a call that the earnings base they are building is real, and that real earnings bases eventually get priced.

Until then, we wait. Patience is not a strategy on its own. But patience attached to good businesses bought at sensible prices is, in our experience, the single largest source of returns in this segment of the market.

If you would like to better understand our framework, you may write to us at gaurav.a@nineonecapital.in or fill in the form here (link).

Couldn't agree more with the thesis here.. I guess it takes conviction in ones own past prudence to weather out present day turbulence. 👍😅

the fantastic writing ..