How Our Screening Process Identified Narayana Health at an Inflection Point

How consistent screening, not consensus, led us to one of our top performing holdings.

In public markets, process trumps prediction. While narratives get attention, it is repeatable frameworks that quietly deliver long term outperformance.

At Nine One Capital, we follow a disciplined and data driven approach to uncover mispriced opportunities through regular sector screening. Every quarter, we update key P&L metrics trailing 12 month (TTM) revenue, EBITDA, EBIT, PAT and Networth across our coverage universe. In addition, every six months, we refresh debt and cash figures to arrive at the latest enterprise value (EV). As stock prices change and market caps update in real time, this framework allows us to continuously track critical valuation parameters such as EV/Sales, EV/EBITDA, EV/EBIT, P/BV, and Market Cap/Sales. This helps us monitor sectoral valuation trends, detect anomalies, and identify compelling investment opportunities ahead of the market.

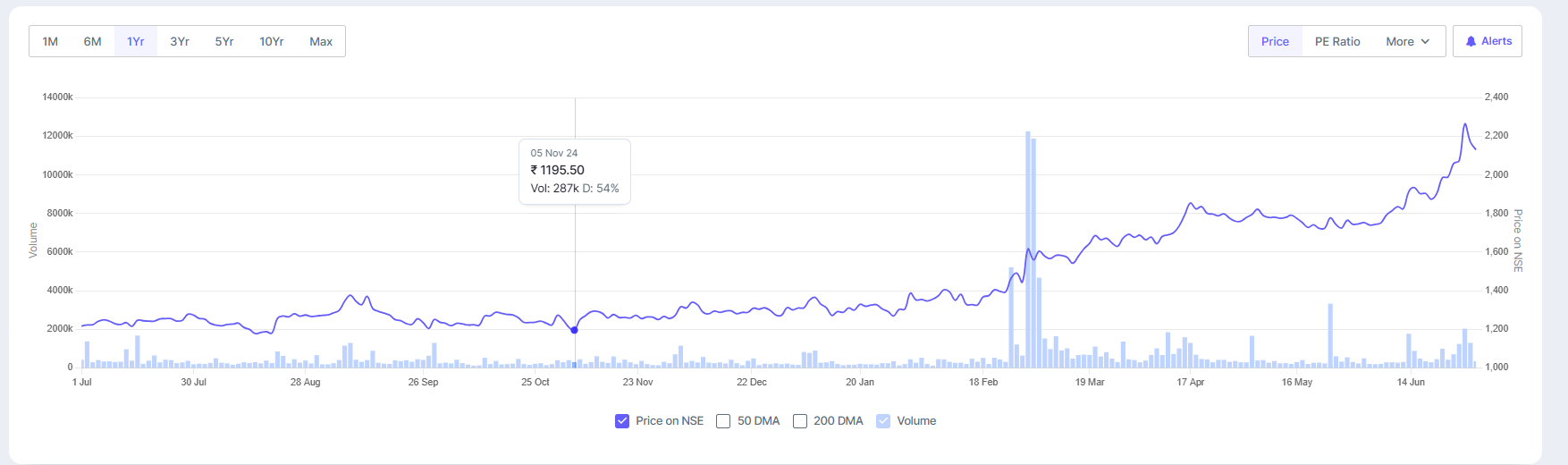

In one such routine exercise last year, our healthcare screens flagged Narayana Health, one of India's leading healthcare providers, as notably undervalued. Despite being widely acknowledged for operational excellence and quality healthcare delivery, Narayana Health was surprisingly trading in the lower quartile of its sector peers. Below is the snapshot from that screen as on Nov 2024 post the Q2 FY25 results:

As shown in our sector valuation screen, Narayana Health was trading meaningfully below the median valuation for listed healthcare delivery companies, around 30x at that time. This anomaly immediately caught our attention and prompted a deeper dive into the company’s investor presentations and earnings call transcripts.

While the underlying fundamentals were strong, consensus sentiment was muted. Sell side reports and conversations with buy side peers revealed a common concern: Narayana lacked visible near term growth triggers. The company had not added significant bed capacity in recent years, and most of its expansion plans were geared for fruition 2–3 years out, leading many to defer interest until growth became more visible.

But for us, this long gestation period aligned perfectly with our typical investment horizon of 3 years. We saw an opportunity to buy one of India’s most respected hospital franchises at a very reasonable valuation, precisely at a time when near term skepticism was creating a favorable risk reward setup.

More importantly, the earnings call highlighted a series of operational initiatives that were likely to improve asset productivity and margins even before the new capacity came online. In essence, the company was creating internal levers for profitability growth, even in a period of modest topline expansion. Some of the key developments discussed in the public domain included:

Cayman Facility Expansion: Commissioning of the outpatient facility in Cayman, with full scale hospital operations expected shortly, setting the stage for a new revenue stream.

Greenfield Expansion in India: Around 1,500 beds to be added across Kolkata, Bangalore, and Raipur over the next 3 to 4 years expanding presence in strategic locations with high demand.

Operational Efficiency Drives: Investments in proprietary platforms like ATHMA (hospital operating system) and Medha (AI driven analytics) aimed at improving workflow automation, cost controls, and decision support.

High End Procedural Growth: A sharp focus on complex, high margin procedures such as robotic cardiac surgeries and advanced oncology driving up revenue per patient and enabling better capacity utilization.

In our view, this was classic perception vs. reality mispricing. The market was overly focused on the near term bed addition gap and missing the broader picture: a high quality hospital platform, building long term capabilities, with improving margins and optionality on future growth.

To corroborate company’s version and figure out if we are missing out anything, we spoke to couple of industry people. We received a positive feedback. This thesis led us to initiate a position and eventually scale it into one of our top five holdings.

As evident above, Narayana Health saw a sharp valuation rerating as the company delivered on its promises: enhancing productivity, expanding margins, and demonstrating a disciplined, profitability first approach to growth. Here is how the screen currently looks like:

Instead of chasing aggressive bed additions, management focused on “doing more with the same space,” prioritizing operating leverage and asset efficiency over headline expansion. We encourage our readers to go through the latest presentation and con call transcript of the company to gain better insights on company’s topnotch execution.

Why We Trust Sector Level Valuation Screening:

Returning to the process that helped us identify Narayana Health at a critical inflection point. Our quarterly sector screening framework plays a central role in how we generate ideas, build conviction, and allocate capital.

Proactive Idea Generation: By scanning sector valuations regularly, we’re able to surface mispriced opportunities well before they come into mainstream focus.

Objective Framework: Removes emotional biases and ensures decisions are grounded in quantitative analysis, reducing impulsive or subjective investment moves.

Market Awareness: Consistently tracking sector valuations provides valuable insights into emerging trends, cyclical shifts, and investor sentiment changes.

Comparative Clarity: Benchmarking companies within their peer group clearly highlights outperformers, underperformers, and opportunities hidden beneath industry wide valuation trends.

Efficient Capital Allocation: With a dynamic understanding of risk reward across sectors, we can rotate capital into ideas with superior upside and better margin of safety.

This disciplined, data driven approach remains central to our investment philosophy. It not only generates compelling investment opportunities but also reinforces our conviction, helping us stay patient and invested during volatile market phases. More importantly, it allows us to identify asymmetric opportunities where the downside is limited but the potential upside is significant. These rare low risk, high reward setups that can materially drive long term returns.

Thanks to this process driven approach and investment discipline, our portfolio has consistently outperformed benchmark indices while maintaining lower drawdowns and generating superior risk-adjusted returns.

Important Note and Disclaimer: Please note that this note is shared only for the education purpose and in no way, it constitutes any buying or selling recommendation. We currently hold Narayana Health in our portfolio.

If you are interested in accessing our research and joining a network of well informed investors, please contact us at Gaurav.a@nineonecapital.in

saw similar pattern happening in P I Industries happening few weeks back.

Narayan Narayan