Looking at the Logistics Sector

India's logistics sector may be approaching an inflection point

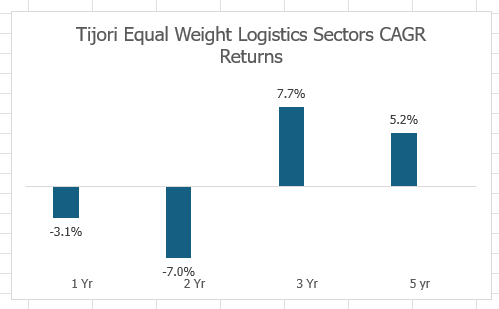

The logistics sector has underperformed over the past 5 years, largely for reasons external to it. Red Sea rerouting lengthened voyages and disrupted sailing schedules through 2024 and 2025; the West Asia escalation and the disruption around the Strait of Hormuz this year have weighed directly on India’s EXIM volumes. Freight rates have been volatile, trade flows soft, and reported earnings across the listed space reflect this. Valuations have compressed accordingly.

Our framework when a sector is out of favour is to separate cyclical drivers from structural ones. The current volume weakness is cyclical and externally driven; it will normalise on a timeline no company in the sector controls. Against that, the sector is in the middle of absorbing its most significant infrastructure addition in decades, the Dedicated Freight Corridors (DFC), which is built, funded, and now substantially commissioned. In our experience, periods where cyclical weakness coincides with structural improvement are worth the work, because the market tends to price the cycle more efficiently than it prices the structure.

Within the overall logistics as a sector, one has an option to play the sector via express, trucking, 3PL, warehousing, cold chain, shipping, ports. We have concentrated on rail-linked container logistics: container train operators (CTOs), Inland Container Depots (ICDs) and Container Freight Stations (CFSs). This is where the structural change is concentrated, and where the dispersion between winners and losers is likely to be widest. This note covers the industry framework and company-specific work is happening as we write this note.

We will start this note with the explanation of a decipher a couple of terms so that the reader also appreciates the overall story.

The container chain in brief

Consider a standard export movement. A manufacturer near Ludhiana stuffs a container that must reach a vessel at Jawaharlal Nehru Port (JNPT, Nhava Sheva), roughly 1,400 km away, clearing customs en route. The cargo owner has two options: road for the full distance, or rail for the line-haul with road at either end. Most of the economics discussed below concern the competition between these two modes on long-haul EXIM lanes.

One unit of measurement to establish: the industry counts volumes in TEUs which is essentially twenty-foot equivalent units. A 20-foot container is one TEU; a 40-foot container is two. When an operator reports throughput of 750,000 TEU, that is the volume line of the business, and most unit economics (realisation per TEU, EBITDA per TEU) are expressed against it.

Inland Container Depots (ICDs): An ICD is a dry port, an inland terminal with rail sidings, container yards, warehousing and a customs presence. Cargo is customs-cleared at the ICD and moves to the gateway port as bonded cargo, ready for direct loading. The ICD operator earns terminal handling, storage and warehousing income, customs-linked service fees, and first/last-mile road transport margins on each box. Where the operator also runs the trains, rail freight is the largest revenue line. Well-located ICDs with surplus land can add capacity at low incremental capex, which supports returns through the cycle.

Container Freight Stations (CFS): A CFS performs a similar function at the port gate: import containers are evacuated from the terminal to the CFS for examination, de-stuffing and delivery, and exports are aggregated there. Revenue comprises handling charges, ground rent on dwell time, and transport. Dwell time is the key revenue driver, the business has historically monetised the gap between the speed at which vessels discharge and the speed at which customs and consignees take delivery. This is an important point to note.

ICD vs CFS quickly: Same job, different postcode: an ICD is a piece of the port relocated 1,400 km inland to where the factories are; a CFS is a piece of the port pushed just outside its own gate to keep the terminal moving.

Container train operators: Private operators have run container trains on the Indian Railways network under long-term licences since 2006. The operator owns or leases rakes (one rake carries roughly 90 TEU loaded single-stack), pays Indian Railways a haulage charge for track and traction, and prices the customer on a door-to-door basis. Realisation on the north India–west coast EXIM lanes runs at approximately ₹20,000–21,000 per TEU. The margin is the spread between that realisation and the haulage, handling and road costs beneath it. Two variables dominate the spread: asset utilisation, since a rake is a largely fixed cost; and empty running, the repositioning of empty containers and rakes against unbalanced trade flows, which is the principal source of margin leakage in the system. Operators that run balanced corridors with high load factors earn meaningfully better unit economics than headline volume growth would suggest.

For orientation, the listed landscape includes CONCOR (the public-sector incumbent and largest operator by a wide margin), Gateway Distriparks (the largest private CTO, with a rail-linked ICD network in the north-west), the Adani ports-and-logistics complex on the Gujarat coast, and Allcargo Terminals (the largest CFS operator). These are referenced to map the industry, not as recommendations.

The Dedicated Freight Corridor (DFC)

The starting point is why rail persistently lost share to road on long-haul container traffic despite a lower cost per tonne-km. Freight trains shared track with passenger services and received lower priority; average speeds were low and transit times unreliable; and double-stack operation was not possible under standard overhead electrification on the trunk routes. The binding constraint was reliability, not price. A shipper choosing between a truck with a dependable three-day transit and a train with a variable three-to-six-day transit generally chose the truck.

The DFC addresses this directly. The Western DFC is a freight-only corridor of approximately 1,506 km from Dadri in the NCR to JNPT, engineered to a different specification from the mixed-traffic network: 25-tonne axle loads, train lengths up to ~1.5 km, design speeds of 100 km/h, and overhead electrification raised to 7.57 metres, sufficient to run double-stacked container trains under electric traction. India is the first railway globally to operate double-stack container services under electrified overhead wire.

The economics of double-stacking are straightforward. The fixed costs of a train path, locomotive, crew, the haulage slot itself, do not scale with the second tier of containers, so a double-stack service carries close to twice the TEUs per path at an estimated 25–35% lower cost per TEU on the rail leg.

The corridor’s remaining gap had been the final connection into JNPT itself. Until that link was complete, double-stack services from the North India either terminated short of the country’s largest container port or routed to the Gujarat ports (Mundra, Pipavav), which already had corridor connectivity. That last-mile link is now live which was slated to open originally in Dec 2023. The practical consequence: end-to-end double-stack operation from the NCR ICDs to JNPT, with line-haul transit compressing from three to four variable days to approximately 24–30 hours on a reliable schedule.

What it changes

First, this is a share story, not a pricing story. The intuitive read, that operators capture the double-stack saving as margin, is incorrect. Rail competes with road, and operators compete with each other; the majority of the cost saving will be passed to shippers, because that pass-through is precisely what drives the modal shift. The relevant metric is the rail coefficient: the proportion of containers at the port moving by rail. At JNPT this has been approximately 15% for years; incumbent operators are now guiding toward 30%+ over a three-to-five-year horizon. The opportunity for operators is volume and share. The genuine margin lever is operational - higher load factors, faster rake turns, and lower empty running as corridor volumes balance. We would monitor EBITDA per TEU rather than headline margins to test whether unit economics are holding through the ramp.

Second, the benefit is corridor-specific. The economics improve for origin-destination pairs on the alignment, NCR, Punjab, Haryana, Rajasthan and Gujarat, to and from JNPT, Mundra and Pipavav. Cargo originating in the south or east is largely unaffected at this stage. The DFC is not a sector-wide re-rating event; it is a lane-specific one, and exposure to those lanes is the first screen we apply to any company in the space.

Third, the hinterland consolidates around rail-linked nodes. As the rail leg becomes faster and cheaper, cargo within a 150–200 km radius of a corridor-linked ICD has a stronger economic case to aggregate there, and warehousing capacity tends to follow. ICD owners with established terminals and expansion land on the corridor benefit from a long-duration tailwind that is independent of any single freight cycle.

Sub-segment implications

Beneficiaries: Container train operators aligned to the corridor capture the share shift — the incumbent through scale, the private operators with greater operating leverage to incremental volumes given their smaller base. Rail-linked ICDs on the corridor compound the throughput growth. Both gateway port clusters benefit: JNPT recovers northern hinterland cargo it had been ceding, while Mundra and Pipavav retain the advantage of earlier connectivity. Ancillary demand for wagons and terminal equipment follows the fleet expansion.

Pressured: The port-side CFS segment faces two concurrent headwinds from the same efficiency drive. Direct Port Delivery (DPD) under which accredited importers take containers directly from the terminal, bypassing the CFS which already accounts for a meaningful and policy-supported share of import volumes at the major ports. Separately, faster rail evacuation reduces dwell time, which is the CFS’s primary revenue driver. The segment’s addressable volume can therefore shrink even as port throughput grows. Long-haul trucking on the trunk corridor also cedes share, although road retains first/last-mile movements, shorter hauls, and all off-corridor lanes.

Largely unaffected. Express logistics, e-commerce fulfilment, contract logistics and cold chain operate on different demand drivers. The DFC is not a thesis for owning them, and the current EXIM weakness is not the primary risk to them. Keeping these sub-segments analytically separate is, in our view, necessary to avoid paying for a tailwind a business does not have.

Way Forward

We are tracking a set of companies across the three sub-segments — the train operators, the ICD owners, and the CFS operators, where the relevant question is whether the structural pessimism is now overdone — and are working through their business models, unit economics and balance sheets.

In summary: a sector cyclically depressed by external events, a structural infrastructure change reaching completion, and a small set of business models with direct exposure to the specific corridor where that change applies. That combination is, in our view, a reasonable starting point to spend more time on researching these companies.

At Nine One Capital, we spend a significant amount of time building the right analytical foundation before forming a view on any company. If you would like to understand our research process in more depth or explore how our advisory services can support your investment journey, you can reach us at gaurav.a@nineonecapital.in or fill in the form here (link).

Disclaimer: Nine One Capital is a SEBI Registered Investment Adviser (Registration No. INA000018814). This article is not a buy/sell recommendation. We are simply highlighting our process of evaluating results based on publicly available data. We could be wrong, and investors must do their own due diligence before taking any position. Please note that this note is shared only for the education purpose and in no way, it constitutes any buying or selling recommendation. We do not hold positions in the companies discussed above.

Have you looked at Sical logistics? Promoter changes have happened at the company. They also have good order book in hand.