Our Forensic Process in Action: The Reality Behind a Narrative-Driven “Deep Tech” Story

A live case study in identifying non-obvious governance, legal, and cash-flow risks beyond conventional market analysis

Disclaimer: This note is based on a real forensic diligence exercise undertaken by our firm. Company names, locations, and identifiable details have been anonymized to focus on process, red flags, and analytical judgment.

__

Bull markets have a peculiar habit. Narratives begin to travel faster than facts.

Every cycle has its chosen themes. In the current one, Semiconductors, Defence, and Deep Tech dominate investor imagination. Scarcity of listed plays, combined with policy tailwinds and global headlines, has created fertile ground for story stocks, particularly in the micro- and small-cap universe.

It was against this backdrop that we evaluated what appeared, at first glance, to be a textbook beneficiary of this enthusiasm. For the purposes of this note, let us refer to it as Company X.

On paper, Company X was a legacy software business with modest but steady operations. Management announced a strategic pivot into high-end s************ manufacturing, positioning itself as a domestic champion aligned with global supply-chain realignment. They released glossy presentations claiming investor presentations claiming:

Internal accruals funding capital-intensive fabs

Strategic technology partnerships

Export ambitions targeting the US and Europe

Predictably, the stock attracted attention. Liquidity picked up. The narrative found its audience.

As our readers/ clients would know, at our firm, we do not invest in narratives. We invest only after they have survived our process oriented research and forensics framework. While the “Street” was reading the company’s press releases, our proprietary Forensic Engine was scouring global sanctions lists, US federal court dockets, and obscure balance sheet footnotes. Here is how our unique process uncovered a minefield that standard analysis completely missed.

1. The Loudest Red Flag Was Silence

The first and most glaring red flag wasn’t what we found, it was what the company didn’t disclose.

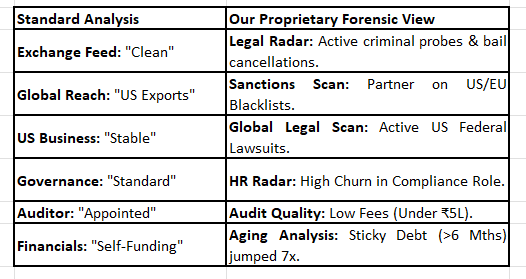

Under standard regulations, material events, like the arrest of a key promoter or a catastrophe at a sister concern should be disclosed. Yet, when we looked at the exchange feed for Company X, we saw only “Strategic Partnerships” and “Growth” updates.

What Our Proprietary Tools Uncovered: Our Regulatory Radar, which tracks real-time police FIRs and court orders beyond the exchange, flagged a massive discrepancy.

The Event: A separate industrial entity, owned and controlled by the same Promoter family, had suffered a catastrophic explosion due to the alleged illegal storage of hazardous materials.

The Legal Fallout: High-level court orders revealed that bail had been cancelled for key leadership figures, with central agencies seeking custodial interrogation regarding customs evasion.

The Edge: Standard financial screeners showed a “clean” company. Our tools revealed a management team distracted by active criminal proceedings and reputational contagion.

2. The Sanctions Reality Behind the “Global Partner” Claim

Company X’s entire growth thesis rested on importing sophisticated machinery from the West and partnering with a domestic “high-tech” firm to package chips for global export.

What Our Proprietary Tools Uncovered: We ran the partner entity through our Geopolitical Risk Matrix.

The result: The key technology partner had been placed on the US Entity List and EU Sanctions List just months prior for alleged involvement in dual-use military supply chains.

The Edge: This wasn’t just a “bad partner”; it was a business model failure. Western laws effectively prohibit transferring technology to sanctioned entities. The “Global Export” plan was legally impossible the moment it was announced.

3. Global Legal Exposure: The US Was Not a Cash Cow

Management sold a story of a “Stable Cash Cow” in the US that would fund their risky pivot. Most analysts only check Indian court records. We checked globally.

What Our Proprietary Tools Uncovered: Our cross-border legal scan picked up active litigation in US Federal Courts.

The Findings: We found active lawsuits involving the US subsidiary for copyright infringement and contract disputes.

The Verdict: The “stable” legacy business was actually fighting legal fires abroad, creating a resource drain the Indian filings never mentioned.

4. Governance Stress Signals: When Oversight Becomes Superficial

In our experience, governance failures rarely announce themselves through one dramatic event. They surface instead through persistent fragility in the very roles meant to safeguard compliance and oversight.

At Company X, two such signals appeared simultaneously.

What Our Forensic Review Uncovered: First, there was pronounced instability in the key managerial personnel responsible for statutory and regulatory discipline. Over a span of roughly three years, the company cycled through three different Company Secretaries. This role is not operational; it is fiduciary in nature. Sustained churn at this level is seldom accidental and typically reflects internal tension around compliance standards, disclosure thresholds, or board-level governance practices.

Second, we evaluated the quality of external oversight. For a company projecting itself as a future-facing semiconductor player with global ambitions, one would reasonably expect a Tier-1 audit firm with the depth and skepticism required for complex, capital-intensive businesses. Instead, the statutory audit was conducted by a small individual proprietorship. The audit economics reinforced this concern. Total audit fees were under ₹10 lakh, with the core statutory audit costing less than ₹5 lakh. These numbers are fundamentally inconsistent with the scale, complexity, and global exposure management claimed to be pursuing.

5. Earnings Quality and Liquidity: When Reported Profits Do Not Translate into Cash

The final and most decisive test for any transformation story is simple: does the business generate real, usable cash.

Management positioned the legacy operations of Company X as a dependable cash engine that would internally fund a capital-intensive semiconductor expansion. We therefore shifted our focus away from headline profitability and towards the two areas that ultimately determine financial durability: accounting quality and cash conversion.

What Our Analysis Revealed: A detailed review of capitalization policies revealed an early distortion. While management commentary suggested that R&D expenditure was moderating, the balance sheet told a different story. “Intangible Assets Under Development” continued to rise, indicating that costs which would ordinarily flow through the P&L were being capitalized instead.

We then examined whether even these reported profits were converting into cash. A multi-year debtor ageing analysis produced a far more concerning picture. Receivables outstanding for more than six months nearly doubled as a share of total debtors, rising from roughly 9% to close to 20% in just two years. In absolute terms, cash locked up beyond the six-month mark increased approximately seven-fold, from about ₹2.6 crore to over ₹19 crore.

Summary: The Proprietary Difference

Company X wrapped a futuristic narrative around a toxic core. But the scariest part? None of these risks were visible in the annual report or exchange filings.

None of these risks were visible through conventional screening, headline ratios, or management presentations. They emerged only when the business was examined across jurisdictions, across entities, and across accounting layers.

This is precisely why we remain process-led and forensic-first in our investing approach. In micro- and small-cap markets, the biggest risks are rarely the ones investors debate openly. They sit in footnotes, court dockets, related-party ecosystems, and cash-flow statements, waiting to be ignored.

Capital preservation, in our experience, is earned not by predicting winners, but by systematically eliminating businesses that fail basic tests of governance, cash integrity, and execution feasibility.

For investors who believe that depth is a prerequisite for durable returns, this is the kind of work that underpins every decision we make. If this framework resonates, and if you value research that looks beyond narratives and into realities, we encourage you to contact us at gaurav.a@nineonecapital.in or fill in the form here (link) to discover how our research services can keep you ahead of the curve

In markets full of stories, process is the only real edge.

Important Note and Disclaimer: This article is not a buy/sell recommendation. This note is shared only for the education purpose and in no way, it constitutes any buying or selling recommendation.