Small/ Microcaps Make Multi-Baggers. Then They Take Them Back

Two cycles, 2,196 companies, and the case for being in this segment with discipline rather than generalized multi bagger narratives.

When investors think about small/microcaps, the first image that comes to mind is the multi-bagger. The 10x, the 20x, the small company that quietly grew into a midcap and then a largecap, and the early investor who held through it all. Many stories such as Eicher Motors, Bajaj Finance etc come to mind when investing into this segment.

This is intuitively right. Small companies have more room to grow. A ₹500 crore business can become a ₹5,000 crore business without needing the economy to double, without needing global tailwinds, simply by executing well in a niche. The asset class has produced enough legendary winners to make this thesis feel self-evident.

We have lived inside this universe for over a decade. We know the stories. We have also seen what happens when the cycle turns and the same names that compounded 8x in three years give back 60% in the next eighteen months. So we wanted to go behind the intuition and see the actual numbers. Not to disprove it, but to understand the actual base rates of what this asset class delivers, what it takes back, and where the real edge sits for an investor.

We pulled together two complete cycles of data as discussed below:

The Methodology

We constructed two cohorts to capture two distinct cycles in the Indian market.

Cohort 1 covered the period from January 2014 to February 2020. We took every listed company at the start of the period, sorted them by market cap, and split them into two groups: the top 250 companies by market cap, and everything below the top 250 down to a market cap floor of ₹50 crore. This left us with 874 small/ microcaps in the smaller group. The bull phase ran from January 2014 to Jan 2018. The bear phase ran from Jan 2018 to February 2020. We deliberately stopped at February 2020 to exclude the COVID drawdown, which was an exogenous shock rather than a normal cycle bottom.

Cohort 2 covered February 2020 to March 2026. We took every company listed as of 24 February 2020 and ran the same exercise, again splitting into top 250 and everything below down to ₹50 crore. This gave us 1,322 small/microcaps. The bull phase ran from February 2020 to December 2024. The bear phase ran from December 2024 to March 2026. The bear phase here is only 15 months long, and we do not know whether the cycle has fully bottomed or not.

This gives us two cohorts, two complete bull phases, two bear phases of varying severity, and a combined sample of 2,196 small/microcap companies and 500 large companies. Three views per cohort: upcycle returns, full cycle returns, and peak-to-trough drawdown, lets discuss the findings now.

The Upside Is Real

The first cut of the data validates what investors have been claiming all along. Small/ Microcaps do produce multi-bagger outcomes at base rates that no other asset class in India can match.

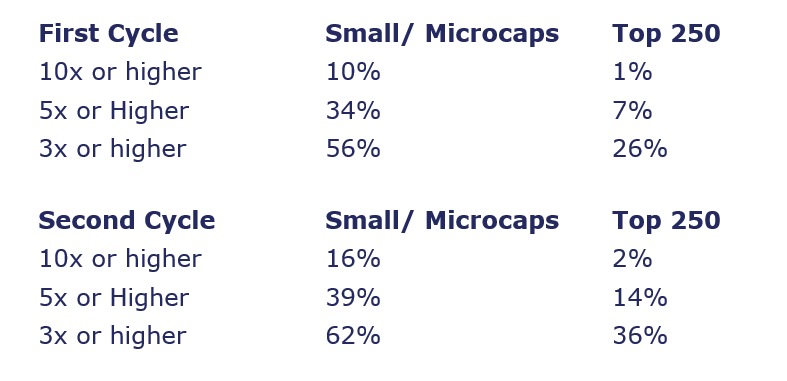

In Cohort 1, of the 874 small/ microcaps, 91 companies delivered a 10x or higher return during the upcycle. That is 10% of the universe. Another 299 companies delivered between 5x or higher and an astounding 487 companies, which is 56% of the universe, delivered at least 3x. The same analysis on the top 250 produced 3 companies delivering 10x, 15 delivering 5x to 10x, and 65 delivering 3x or higher. The base rate of 3x or higher in small/ microcaps (at 56%) was more than double the rate in larger mcap companies(26%).

Cohort 2 was even more extreme on the upside. Of the 1,322 small/ microcaps, 210 companies delivered 10x or higher in the upcycle, which is 16% of the universe. 518 companies delivered 5x or higher. And 814 companies, an extraordinary 62% of the universe, delivered at least 3x. The top 250 in the same period produced 5 companies in the 10x bucket and 89 in the 3x bucket. In the image above, we have given the % of total universe.

The intuitive thesis holds. The small/ microcap universe produces multi-baggers at roughly five to eight times the rate of the top 250 for 10x outcomes, and at roughly twice the rate for 3x outcomes.

The more interesting question is what happens to these numbers when we extend the lens from the peak of the upcycle to the end of the full cycle.

So we ran the same exercise across the full cycle and asked how many of the multi-baggers stayed multi-baggers. The picture changes meaningfully.

The Edge Collapses Without Discipline

This is the cut of the data we found most revealing, and the one we suspect will surprise most readers.

The deeper pattern that emerges when we track the multi-bagger cohort specifically is that the same stocks that ran the most in the bull phase tend to give back the most in the bear phase.

The aggregate numbers reveal exactly this.

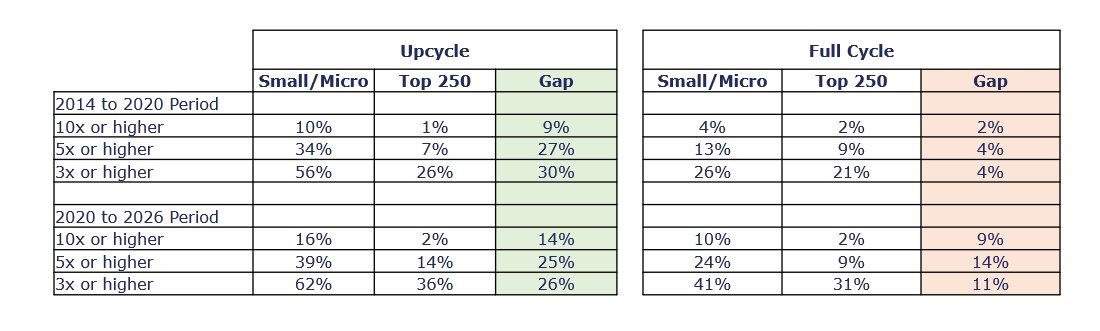

1) In Cohort 1, 56% of the 874 small/microcaps had delivered at least 3x by the peak of the upcycle. Through the full cycle, holding from January 2014 to February 2020, that number collapsed to 26%. The advantage that small/microcaps had over the top 250 in the upcycle was 30 percentage points. Through the full cycle, that gap shrank to just 4 percentage points.

2) In Cohort 2, the upcycle gap was 26 percentage points. The full cycle gap is currently 10 percentage points and likely to compress further if the bear phase extends.

Read that again. The structural advantage of small/microcaps over large caps, on a 3x base rate basis, shrinks from 30 points in the upcycle to 5 points through a full cycle. That is an 83% erosion of the asset class edge for an investor who holds passively.

The 10x bucket fares worse as shown above - what was a 10% probability of hitting a 10x in a bull market became just a 4% probability across the full cycle in the first cohort. The same is true, thought to a lesser extent so far, in the second cohort.

The math here is uncomfortable for the buy-and-hold microcap investor. Most investors who believed they owned a 10x stock never realised it because they held through the cycle. The probability of catching a 10x and keeping it through the next bear is roughly 4 in 100 in Cohort 1, and 10 in 100 in Cohort 2 to date.

Stocks that produce 10x returns are typically stocks where the re-rating got ahead of the earnings, where liquidity drove the last leg of the move, and where narrative compressed the holding period. When the cycle turns, narrative and liquidity unwind at the same time. The entry price the late buyer paid was not justified by the business, only by the trend, and the trend stops paying.

The implication is not that small/microcaps are a bad asset class. The implication is that small/microcaps are an asset class that rewards process and active assessment, not buy and hold. The edge is real. It is just time-sensitive, and it requires the investor to do work that most do not do.

The Downside Is Brutal

If the erosion of the multi-bagger count tells us how much of the upside gets given back, the drawdown data tells us how violently it gets taken away. The two are related, but they are not the same view, and the second one is important because it shapes how an investor actually experiences the asset class in real time.

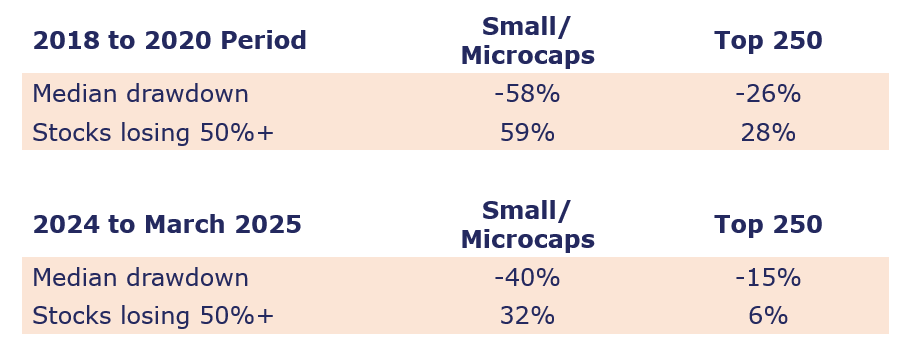

In Cohort 1, the median small/ microcap drew down 58% from its peak to the bear market trough with 59% of small/ microcaps lost half their value or more. The same numbers for the top 250 were a median drawdown of 26% and only 28% of companies losing half their value.

Cohort 2’s bear phase has been milder so far. Median small/ microcap drawdown stands at 40%, with 32% of companies down by half or more. The top 250 median is down 15%, with only 6% of companies losing half.

This is the cost the asset class extracts. The investor who is not prepared for it, or whose entry price did not build in protection against it, is the investor who eventually capitulates and turns the temporary drawdown into a permanent loss.

What This Means for How We Invest

The case for being in this asset class is straightforward. Nowhere else in Indian markets does an investor get a 1 in 2 chance of a 3x in a normal upcycle, alongside the optionality of catching the occasional 10x. Even after the cycle compresses returns, the full cycle 3x base rate of 26% to 41% in small/microcaps is still meaningfully ahead of what large caps deliver, and the wealth created here over the last decade is not an accident of one bull run. The question is never whether to be in small/microcaps. It is how to be in them in a way that captures the edge without surrendering it back.

This is what our practice is built to do. Four filters guide every position we take.

Survive to Thrive. We do not own companies where the books, the promoter behaviour, the auditor history, or the related-party flows fail scrutiny. In a universe where 20% of companies loose 80% in a down market, governance integrity is survival capital.

Valuation discipline. We pay prices that build in protection before the business has to perform. Every position has a defined downside, base, and bull case, and we size on the asymmetry between them. Buying right is what separates a 25% drawdown from a 60% one when the cycle turns.

Cycle awareness. A position that earned its place at one valuation may no longer earn it after a 4x re-rating. We continuously reassess whether the risk-reward of each holding still justifies its weight. This is not market timing. It is portfolio honesty.

Conviction where it is earned. Within this universe there are companies where the right answer is patience, not assessment. Where the business model, governance, and runway justify it, we hold for the long term and back them with weight. These are not many and we know that we will go wrong here. But correctly identified, they are the most powerful contributors to long-term returns.

These four filters compound. The first ensures we do not own capital destroyers. The second ensures we buy at prices that protect us. The third ensures we do not give back what we have made. The fourth ensures we ‘try to’ capture what this asset class is genuinely capable of producing.

The Closing Thought

Small/ Microcaps are one of the most generous asset classes available to an Indian investor. The general perception that they produce multi-baggers is correct. What the general perception leaves out is that the same volatility that creates the upside also takes it back from anyone who treats this segment as buy-and-forget. The investor who passively holds through a full cycle ends up with returns close to large cap outcomes, but with materially higher risk. The investor who applies process, forensic diligence, valuation discipline, and active assessment captures the actual edge.

Small/ Microcaps reward those who respect both the upside and the volatility, the data in this piece is the reason we have built our practice the way we have. If you would like to understand our research process in more depth or explore how our advisory services can support your investment journey, you can reach us at gaurav.a@nineonecapital.in or fill in the form here (link).

Good point.

I would really appreciate another post on the selling framework at Nine One if possible.

good read