When ‘Bad Governance’ Is Not Getting Worse: Lessons from 12 Years of Data

Findings from 12 years of related-party data on cycles, sentiment, and a case where investors are double-counting the already known risk

Related party transactions (RPTs) are often treated as a binary filter in Indian equity markets. A company is either considered “clean” or deemed “uninvestable.”

In practice, this framing misses the point.

What matters far more than the existence of RPTs is context, direction, consistency, and economic behaviour over time. Governance risk is rarely revealed in a single year. It manifests gradually, across cycles, and most clearly during periods of stress (One reason why we try to avoid newly listed companies).

In a recent investment report that we prepared on a cyclical business, we analysed 12 years of related party transaction data to answer a simple but under-asked question:

Are governance risks getting worse, or are they merely persistent and already well understood by the market?

We believe this distinction matters far more than most investors realise. We are sharing our framework publicly because it reflects how we think about governance, not just what we concluded in one specific case.

Why We Look at 10–12 Years, Not 2–3

Governance analysis conducted over short time horizons is often misleading, especially in cyclical businesses. Cycles distort financial optics in predictable ways. During downcycles:

Profits collapse rapidly due to operating leverage,

Working capital expands as volumes slow and pricing weakens,

Debtors rise as stress propagates through the ecosystem, and

Long-standing governance concerns resurface with renewed intensity.

None of this necessarily indicates that the business has changed. More often, it reflects stress revealing fragility, not behavioural deterioration.

A common mistake investors make is to treat cyclical stress signals as structural shifts. One or two bad years, viewed in isolation, can easily be interpreted as evidence of “business with bad fundamentals” when in reality the business is simply at the wrong point in the cycle.

This is why short-window governance analysis is dangerous. It systematically overweights bad years and underweights context.

Long-term data, by contrast, allows us to separate:

Structural behaviour, which persists across cycles, from

Cyclical stress responses, which emerge predictably during downturns and recede as conditions normalise.

In our work, we deliberately studied a full upcycle–downcycle–upcycle sequence. This is the only reliable way to assess whether governance issues are increasing or the same as before.

What We Analysed (and Why)

In the case we studied, one of the market’s central concerns revolved around related party transactions with promoter-owned entities. This concern has been repeatedly raised by investors and analysts, including in the recent earnings call.

To get a context, it is important to see how these transactions have evolved over the years and across the cycles to get a context whether things are same as before or worsening.

Our framework did not attempt to assign moral judgments or label governance as “good” or “bad.” That approach is neither practical nor particularly useful for capital allocation.

Instead, we focused on directional behaviour. Specifically, we examined:

Related party sales as a percentage of total revenue,

Related party debtors as a percentage of total debtors,

Debtors relative to related party sales,

External (non-related party) debtors relative to external sales, and

How each of these variables behaved during upcycles versus downcycles.

The objective was not to prove cleanliness. The objective was to access whether the extent of RPTs are same or increasing in the overall proportion of the business. In investing, widely known issues are usually already discounted in the price. Risk, in our framework, is defined by deterioration.

The Findings

Based on the last 12 years of annual reports, we tried to establish a pattern using the below format:

1. Related Party Sales Are Structurally High, but Not Deteriorating

Related party sales have remained elevated at ~30–40% of revenues for more than a decade. However, there is no evidence of a secular upward trend.

Recent levels are broadly in line with long-term averages and well within the historical range. In other words, the company’s dependence on its broader promoter ecosystem has been persistent, not progressive. Persistence implies a known, stable structure that markets can price. Deterioration implies incremental risk that warrants valuation impairment. The data supports the former, not the latter.

2. Debtor Concentration: A Permanent Policy, Not a New Risk

Investors often react with alarm to the fact that ~90% of the company’s debtors are related parties. However, our 12-year longitudinal study shows this has been the status quo even during “goldilocks” periods.

The Upcycle Context: In FY21–22, when the company traded at premium valuations (~6–7x P/BV), RP debtor concentration was almost identical to today’s levels.

The Logic: This concentration is actually the inverse of the company’s ultra-conservative third-party credit policy (see Finding #4). The market has previously accepted this concentration when earnings were strong; to reprice it as a “new” governance failure now is a logical inconsistency.

3. Debtor Intensity: A Cyclical Liquidity Buffer

While the concentration (who owes money) is stable, the intensity (how much they owe relative to sales) is cyclical. Debtors as a percentage of RP sales have recently risen to ~45–50%, up from a historical average of ~30%.

This suggests that during poultry downcycles, the listed entity acts as a liquidity buffer for the broader promoter ecosystem. While this isn’t “ideal” governance, the data shows that these balances have historically expanded during stress and normalized rapidly as operating conditions improved.

Our research indicates that the Parent level liquidity is very strong (estimated at ~₹1,000 Cr), this “trapped” working capital represents a massive, unpriced cash-flow catalyst for the next upcycle.

4. External Receivables Quality Is Exceptionally Strong

Perhaps the most underappreciated finding lies outside the related party ecosystem.

Debtors excluding related parties are just ~2% of ex-related party sales, effectively resembling cash sales. For context, the company has approximately ₹44 crore of external debtors on outside revenues exceeding ₹2,300 crore.

This highlights:

Strong pricing power,

Tight credit discipline, and

No evidence of stress being pushed onto third-party customers.

This is a critical counterbalance to headline concerns around working capital and speaks to the underlying operational quality of the business.

5. No Evidence of Structural Deterioration in RPT Behaviour

Taken together, the data points to governance stagnation, not governance decay (explained in the next section). There is no material evidence of:

Increasing economic leakage,

Worsening transaction intensity beyond historical ranges, or

Erosion of minority shareholder economics over time.

The behaviour observed in the current downturn is consistent with prior cycles, not indicative of a new or worsening governance.

Governance Decay vs Governance Stagnation

This distinction is critical.

Governance decay occurs when behaviour progressively worsens over time, economic leakage increases, and the economic claim of minority shareholders erodes. This warrants permanent valuation impairment.

Governance stagnation occurs when the same issues persist, are well known, well disclosed, and resurface emotionally during periods of stress, but do not structurally intensify.

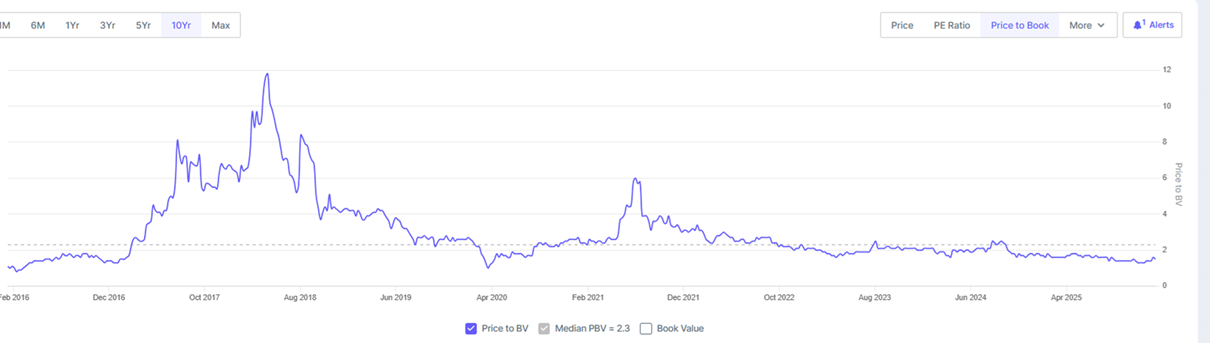

In the case we studied, the data overwhelmingly indicates to Governance Stagnation. The patterns observed during the current downturn were not new. Similar behaviours existed in prior cycles, including periods when the market was willing to assign materially higher valuation multiples as shown in the below historical P/Bv chart (taken from screener)

What changed was not governance behaviour. What changed was sentiment. The market reaction appeared driven by cyclical pessimism layered on top of long-standing concerns, not by fresh evidence of deterioration.

Beware of Cyclical Bottoms

Investors tend to make two mistakes simultaneously at cycle bottoms:

They extrapolate trough earnings as if they represent a new normal.

They reprice unchanged risks as if they are newly discovered.

When these two forces combine, valuation compression can become excessive. This is precisely how mispricing emerges in cyclical businesses with known imperfections.

The opportunity does not come from pretending the risks do not exist. It comes from recognising when the market is double-counting them. In the case we analysed, similar levels of related party transactions existed in prior cycles when the company traded at meaningfully higher valuation multiples.

Conclusion

This post deliberately focuses on just one part of a much larger research effort since this aspect is least talked about and is the most misunderstood. In our full report, we go far beyond governance and related party transactions. We analyse:

How the business is structured across segments and where cyclicality is created versus absorbed,

How profitability behaves across normal and super-normal phases, not just during downturns,

Balance sheet resilience and capital allocation choices that determine survivability,

Valuation frameworks, return asymmetry, and position sizing discipline, and

The complete risk matrix, including both operating and governance risks.

As always, the intent of this note is to share our thinking framework, not to make investment recommendations.

At Nine One Capital, we spend a disproportionate amount of time studying how expectations are formed, and how markets repeatedly misprice risk and recovery across cycles. Much of our work focuses on separating what has actually changed from what merely feels different during periods of stress. For readers interested in understanding our research approach in greater depth, or in exploring how our advisory services may support their long-term investment decision-making, you may write to us at gaurav.a@nineonecapital.in or fill in the form here (link).

Important Note and Disclaimer: This article is not a buy/sell recommendation. This note is shared only for the education purpose and in no way, it constitutes any buying or selling recommendation.

The key takeaway for me is that governance risk should be evaluated directionally, not emotionally. Without evidence of deterioration, markets may end up penalizing persistence as if it were decay — leading to mispricing.