Working with Limited Information: BN Holdings Reverse Merger

Dissecting the BN Holdings Merger Through Numbers, Not Narratives

In the dynamic world of public market investing, complete information is often a luxury. Investors frequently have to make educated assumptions and informed guesses, knowing that waiting for clarity may mean missing out on attractive entry points. Last weekend, we came across a particularly intriguing event: the scheme of amalgamation involving BN Holdings, which is reverse merging its promoter entities into the listed entity. Given the limited details available, we undertook a thorough yet assumption-driven analysis to evaluate the risk-reward profile. Here's our detailed thought process and findings.

The Scheme

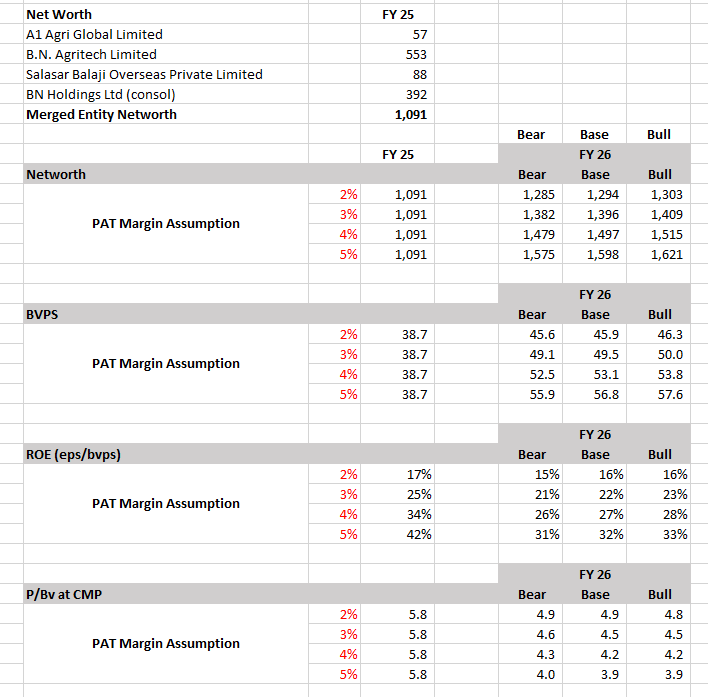

On June 28, 2025, BN Holdings announced a reverse merger involving three promoter-owned entities: A1 Agri Global Limited, B.N. Agritech Limited, and Salasar Balaji Overseas Private Limited, into the listed entity BN Holdings. Here's a snapshot of each entity:

BN Holdings Limited (Listed Entity): Primarily involved in investments in companies engaged in the manufacturing and trading of edible oils, oil seeds, solvent extraction, and refined oils.

A1 Agri Global Limited: Specializes in manufacturing and trading edible oil. FY25 Turnover: ₹1,494 crore; Net Worth: ₹57 crore.

B.N. Agritech Limited: A leading edible oil manufacturing player in North India. FY25 Turnover: ₹6,280 crore; Net Worth: ₹553 crore.

Salasar Balaji Overseas Private Limited: Engaged in the wholesale and retail trade of agricultural produce. FY25 Turnover: ₹1,151 crore; Net Worth: ₹88 crore.

The merger is aimed at operational efficiency, centralized procurement, better inventory management, and optimized working capital management. The promoter holding in BN Holdings will increase significantly post-merger, indicating strong promoter alignment.

Financial Assumptions and Valuation Approach

Given that detailed profitability figures weren't available, we used revenue data from the scheme document and assumed various PAT margins (ranging conservatively from 2% to optimistically 5%) to estimate the resulting entity's EPS.

Note that the scheme document has given total assets and in these three companies Revenue/ Total assets is 4 to 6x which means low value addition and hence we thought 2-5% PAT range is optimal. One can take higher PAT margins to do this but in our experience being conservative is a better choice.

Additionally, considering typical growth dynamics in agri-commodities, we applied annual revenue growth assumptions of 5-15% to arrive at FY26 earnings scenarios. Post reverse merger number of shares are provided in the document. One can access this document here.

Earnings and Valuation Matrix

With our EPS scenarios, we analyzed the resultant PE multiples under two broad pricing assumptions:

At the Current Market Price (CMP).

At a 50% discount to CMP (creating an attractive margin of safety).

This approach gave us clarity on valuation comfort across various growth and margin outcomes. (Refer to attached valuation matrix image).

Let’s see this with 50% discount to CMP while keeping all other things same:

Our sensitivity analysis clearly highlights the interplay between assumptions and valuations. At the CMP of ₹224, valuations seem stretched unless one firmly believes in optimistic margin scenarios (4 to 5%) coupled with strong revenue growth.

However, at a hypothetical 50% discount to the CMP (₹112), the risk-reward dramatically improves. Even under conservative growth and margin assumptions, the valuation multiples become quite attractive, significantly tilting the odds in investors' favor.

Book Value and ROE Analysis

Using similar assumptions, we calculated the resultant Book Value Per Share (BVPS) and corresponding Return on Equity (ROE) for FY26, providing additional valuation insights.

As shown above, even under the conservative (bear) scenario, the merged entity displays a robust Return on Equity (ROE) profile of around 15-16% (assuming 2% PAT margin), underscoring inherent business efficiency and profitability. Yet, while the ROE appears healthy, investors must also consider valuation multiples critically. At the Current Market Price (CMP), investors would be paying ~5 times book value, which appears steep for a commoditised business potentially growing at a moderate rate of 10-15% (which is again our assumption).

Risk Reward at Different Price Levels

Investors can further evaluate different PE and P/BV multiples at varying price assumptions to pinpoint attractive entry levels where the risk-reward profile distinctly shifts in their favor, provided they gain comfort around the business model, growth trajectory, and profitability dynamics.

We would have been more inclined to explore this opportunity further had the stock been trading at single-digit PE multiples in the base case and no more than 1.5x book value. levels that would imply a price closer to ₹100, which, notably, was the case just a few months ago. However, given the sharp rally in recent months and elevated valuations even under optimistic assumptions, we do not find the current setup compelling enough to warrant deeper investigation at this stage. That said, we will continue tracking the story and reassess if more substantive information emerges or if valuations reset to more reasonable levels.

Conclusion

We hope that the above analysis helps our readers gain perspective on how to approach investing when information is sparse, something that’s more the norm than the exception in Indian small and micro caps. The idea is not to shy away from such situations, but to apply a structured framework of assumptions, base case and bear case modeling, and valuation sensitivity to arrive at informed conclusions. This approach allows investors to act with rationality rather than be swayed by stories, sentiment, or momentum.

In this case, rather than getting carried away by a reverse merger narrative or the steep recent price rally, we grounded our assessment in numbers, however limited, and built a valuation map to see what levels could offer a compelling risk-reward. The key, as always, is to avoid the trap of FOMO and anchor decisions on valuation, not noise. As markets get more speculative and narratives more seductive, this discipline becomes our biggest edge.

Important Note and Disclaimer: Please note that this note is shared only for the education purpose and in no way, it constitutes any buying or selling recommendation. We do not hold BN Holdings in our portfolio.

If you are interested in accessing our research and joining a network of well informed investors, please contact us at Gaurav.a@nineonecapital.in